Walking the net zero talk: Easy to claim, hard to verify

The system for assessing the promises in companies' climate commitments is not yet fit-for-purpose, write Vitali Alexeev, Katja Ignatieva and Désirée Lucchese

In February this year, the Federal Court dismissed a case brought by the Australasian Centre for Corporate Responsibility (ACCR) against oil and gas producer Santos – the first legal challenge anywhere in the world to contest the credibility of a corporate net zero target. The case had been years in the making. Santos successfully defended it. But the judgment did not validate the substance or credibility of its climate strategy.

It was not Australia’s first greenwashing case. That distinction belongs to ASIC’s 2024 action against Mercer Superannuation, which resulted in an $11.3 million penalty after Mercer admitted to misleading investors about which companies its ‘sustainable plus’ funds actually held. The Santos case is different in kind: it tested not a product label but the integrity of a long-dated net-zero commitment itself.

What the Santos ruling revealed is more troubling than a simple win or loss. As ACCR’s co-chief executive Brynn O’Brien observed, the decision effectively places the burden on investors to "scrutinise every statement, every number and every assumption" behind corporate climate commitments. The legal system examined those claims – and handed the problem back to the market.

This reflects a structural gap that mandatory disclosure alone has not closed: a growing abundance of climate commitments but limited mechanisms to verify their credibility, comparability, or coherence with actual capital decisions.

The disclosure flood has not solved the problem

Australia has moved quickly to strengthen transparency. The Australian Sustainability Reporting Standards (ASRS), introduced in January 2025, require large companies to disclose climate-related risks, strategy, and metrics in a standardised format. Mid-sized firms follow shortly after. The intent is sound: improve comparability, support investor decision-making, and enable accountability.

But more disclosure has not meant better disclosure.

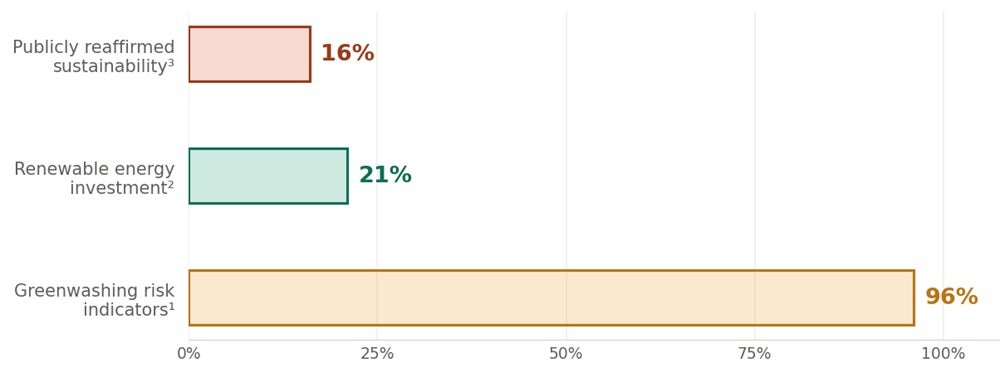

A study published earlier this year in npj Climate Action (the most comprehensive of its kind, covering more than 4000 corporate climate pledges) found that 96% of the companies that pledged exhibited at least one indicator of greenwashing risk. Common red flags included heavy reliance on carbon offsets, exclusion of Scope 3 (supply-chain) emissions, and targets unsupported by credible implementation plans. Crucially, these risk indicators are only weakly correlated with each other. There is no single profile of a high-risk company – and no simple screening method for identifying where the problems lie.

Greenwashing risk indicators

The problem is not primarily misleading reporting. It is more structural and harder to fix. The reporting infrastructure for making climate disclosures and the systems for verifying and assuring those disclosures were never designed to work together in an integrated or consistent way.

The real issue is coherence, not quantity

Strip away the language, and investors want answers to three basic questions: Are the numbers reliable? Does the story hold together? And do financial decisions actually align with stated commitments? None of these is straightforward to answer from a sustainability report alone.

On the numbers, companies still report under a patchwork of overlapping frameworks (TCFD, GRI, IFRS S2), each with different methodologies, boundaries, and assumptions. The IFRS S2 standard, which builds on TCFD foundations, is more prescriptive and better suited to investor decision-making, but adoption is uneven. Two companies in the same sector may publish targets that appear similar but are, in practice, fundamentally incomparable. The recent collaboration between GRI and CDP to align their reporting tools reflects just how fragmented the system remains.

On the narrative, the challenge runs deeper. Sustainability reports combine forward-looking statements, selective metrics, and carefully constructed language. Assessing whether a company’s climate story is internally consistent, across its disclosures, investor presentations, and operational decisions, is difficult using traditional analytical approaches. It requires not just data literacy but robust internal governance and tools capable of systematically identifying inconsistencies across reporting cycles.

On capital allocation, the picture becomes stark. According to BSI’s 2026 G7 Net Zero Temperature Check, a survey of more than 7000 senior business leaders, only 21% of businesses globally have made tangible investments in decarbonisation. At the same time, the median target year for corporate net zero commitments has shifted from 2030 to 2035 since 2021. Commitments are multiplying. Capital is not moving at the same pace.

The credibility gap in climate transition disclosures

The Santos case highlights a deeper truth: climate commitments often rest on assumptions that cannot be verified at the time they are made. A company can set a 2040 net zero target that is legally defensible – reasonable, contextual, disclosed – yet remain practically impossible for investors to assess meaningfully today. The ruling set a legal floor, not a credibility benchmark.

This is particularly pronounced in hard-to-abate sectors such as mining, heavy industry, and transport, where credible transition pathways depend on technologies that are still maturing and on capital commitments that span decades. The International Energy Agency’s 2021 Net Zero Roadmap was unambiguous: no new fossil fuel supply projects are consistent with a net zero pathway. Yet capital allocation trends across several major producers suggest otherwise.

Ultimately, the credibility of a transition strategy is not defined solely by its targets. It is defined by whether capital, operations, and governance decisions align with those targets over time – and whether that alignment can be observed, tracked, and compared by those outside the company.

The counterargument deserves a hearing

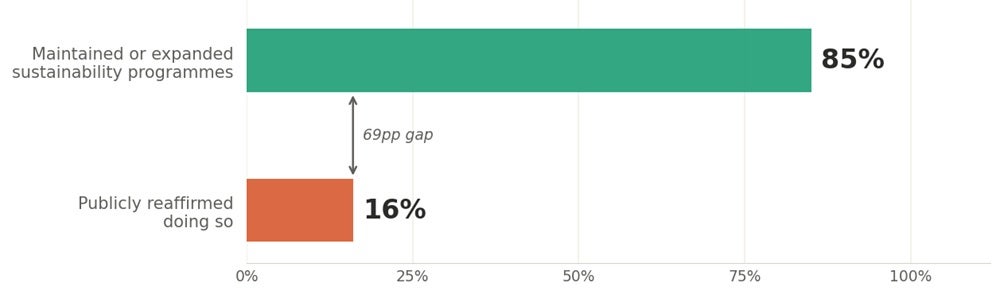

There is a legitimate concern that raising the bar on the verifiability of climate disclosures could have unintended consequences. Companies already wary of litigation may retreat into cautious, non-committal language – saying less rather than more. This phenomenon, widely described as ‘greenhushing’, is real. A September 2025 survey of 75 firms found that while 85% had maintained or expanded their sustainability programmes, only 16% had publicly reaffirmed doing so. Bloomberg Green’s analysis of S&P 500 earnings call transcripts found that mentions of sustainability-related terms had fallen 76% compared to three years prior. The Santos outcome is likely to push some Australian boards in the same direction.

Behind the ‘greenhushing' phenomenon

But the solution is not less scrutiny. It is better scrutiny, focused not on the existence of commitments, but on their internal coherence, scientific grounding, and alignment with observable decisions. The difference between a credible transition plan and a public relations exercise lies precisely in those details.

What needs to change

Three shifts are required, and none depends on the outcome of the next court case.

Investors need to treat disclosures as testable hypotheses, not accepted facts. Assessing credibility requires linking reported emissions and targets to capital allocation, operational decisions, and sector benchmarks. This capability cannot be fully outsourced. It must be built.

Regulators need to move beyond compliance towards comparability and context. Mandatory disclosure is a necessary foundation, but it is not sufficient on its own. Without common methodologies and clearer expectations around assumptions, disclosures risk becoming noise. Placing company disclosures within broader macro and sectoral trends is equally essential.

The gap between narrative and evidence must be closed. The central challenge today is not generating more corporate emissions data. It is developing robust methods and monitoring guardrails to assess whether companies’ transition narratives are credible and aligned with science-based pathways. This means systematically comparing disclosures with observed investments, operational decisions, and, where relevant, lobbying activity. Advances in data analytics, including emerging AI-based frameworks for detecting inconsistencies at scale, offer real promise. But they require careful design and validation. This is an area where academic research plays a critical role.

Subscribe to BusinessThink for the latest research, analysis and insights from UNSW Business School

Where this leaves us

Australia has made genuine progress. Climate disclosure is now mandatory for large entities. Regulators are actively enforcing greenwashing rules. Courts are beginning to test the legal boundaries of corporate climate claims.

But the piece that is still missing is a shared, operational definition of what a credible climate commitment actually looks like: coherent, comparable, and verifiable against the decisions a company makes in practice.

Until that gap is addressed, disclosure will not deliver accountability. And without accountability, the credibility of corporate transition strategies – and the capital that depends on them – will remain in question. Australia has an opportunity to show what genuine climate accountability looks like. The question is whether we use it.

Vitali Alexeev is an Associate Professor in Finance at UTS Business School, Katja Ignatieva is an Associate Professor in the School of Risk and Actuarial Studies at UNSW Business School, and Désirée Lucchese is Head of Climate and Impact, Impact Alpha Partners; Technical Expert Group Adviser, RIAA; and Honorary Associate at UTS Business School.