Why inflation always comes back to the central bank

Research has found that central bank policy regime changes – not supply shocks, cost-push pressures or price stickiness – drove every major inflation episode since the 1960s

After three rate cuts in 2025, the Reserve Bank of Australia reversed course in February 2026, raising the cash rate to 3.85 per cent as inflation climbed back above its target band. The RBA became the first major central bank to shift from cuts to hikes in the post-COVID cycle. Governor Michele Bullock warned that further increases remained on the table and that “every meeting is live.” It was the kind of policy reversal that generates intense short-term debate – about whether the cuts went too far, whether the hike came too late, and what comes next.

But research from three economists across two continents suggests the more consequential question lay elsewhere: not what the RBA did at any single meeting, but whether its actions over the coming years would amount to a temporary adjustment or a lasting shift in Australia’s monetary policy regime. The distinction, they found, was what separated short-lived price fluctuations from the inflation episodes that defined entire decades.

“For decades, the quantity theory of money has been treated as a classroom relic – a useful abstraction but not a serious guide for modern central banking. The prevailing story of the 1970s blames real shocks and price rigidities, pushing monetary forces into the background,” said UNSW Business School Postdoctoral Fellow in the School of Economics, Dr Han Gao, who co-authored a study that argues that this view is deeply incomplete.

“The quantity theory did not fail. Economists were looking in the wrong place. Once monetary policy regime shifts are brought into focus, the classic links (between money growth, inflation, and interest rates) reappear with striking clarity. The message is clear: money and monetary policy still matter – decisively – for inflation over the medium to long run,” said Dr Gao, who firmly asserted that it is time to bring the quantity theory back into the centre of macroeconomic debate.

What one of economics’ oldest ideas says about inflation

The study, Two illustrations of the quantity theory of money reloaded, was published in the Journal of International Economics and authored by UNSW Business School’s Dr Gao, Professor Mariano Kulish from the University of Sydney, and Professor Juan Pablo Nicolini from the Federal Reserve Bank of Minneapolis and Universidad Di Tella. Their findings challenged the view that inflation is driven by supply shocks, wage pressures and price-setting frictions. Instead, they found that over any period longer than about four years, inflation tracked monetary policy variables – interest rates and money supply growth – with precision.

Learn more: The state of the nation: Key challenges for Australia’s economy

The quantity theory of money holds that inflation is, at its core, a monetary phenomenon. Prices rise when too much money chases too few goods. The theory rests on two key relationships. The first links money growth to inflation: when the supply of money grows faster than economic output, prices rise. The second, known as the Fisher equation, links inflation to interest rates: if prices are expected to increase, investors demand higher interest rates to preserve their real returns. The theory fell out of favour in policy circles, replaced by models focused on output gaps and price stickiness. The researchers set out to test whether both relationships still held.

How the researchers tested the theory across 16 countries

The team examined data from 16 OECD countries – including Australia – spanning the 1960s to the mid-2000s. The period covered the high inflation of the 1970s, the Volcker disinflation of the early 1980s and the low-inflation era that followed. They used a statistical filter to strip out policy cycles lasting less than four years on average, revealing trends in inflation, interest rates and money growth. Across the countries studied, correlations between the theory’s predictions and actual inflation exceeded 0.85 in most cases, with only a few exceptions. Australia’s results were among the strongest in the sample, according to Dr Gao.

They then estimated a new Keynesian model using US data that allowed for, but did not impose, shifts in the central bank’s inflation target over time.

Regime changes in monetary policy drove inflation up and down

The model identified a regime change in US monetary policy beginning in the late 1960s, when the inflation target drifted upward, and a second shift in the early 1980s, when it came back down. The paper found that “the shocks to the target alone can do a very good job at tracking the evolution of the long-run component of inflation in the data.” All other factors – supply shocks, cost-push pressures and price-setting frictions – “only add to short-run inflation fluctuations but fail in capturing the high inflation from mid ‘60s to early ‘90s”.

Without inflation regime change, Dr Gao noted that the correlation in testing the theory is close to zero, which is precisely what the two exceptions in testing the theory – Germany and the Netherlands – reflect.

Subscribe to BusinessThink for the latest research, analysis and insights from UNSW Business School

The researchers also tested whether the degree of price stickiness in the economy – the mechanism at the heart of most central bank models – changed the results. It did not. When they varied the price stickiness parameter across a wide range, the differences in outcomes at the low frequency were relatively small. The conclusion was direct: “inflation fell as a consequence of a regime switch in monetary policy, while price frictions played no substantive role.”

Implications for business leaders making medium-term decisions

The research has implications for anyone planning over a three- to five-year horizon. The authors argued that “a reasonable definition of ‘longer horizon’ is roughly four years” – the time horizon over which monetary policy tightening cycles played out in the United States.

The recent US experience fitted this frame. The Federal Reserve held rates near zero during the pandemic, then raised them to a range of 5.25 to 5.50 per cent by mid-2023. By January 2026, US inflation had fallen to 2.4 per cent – broadly in line with the paper’s prediction that inflation should return close to the 2 per cent target within four years of a tightening cycle.

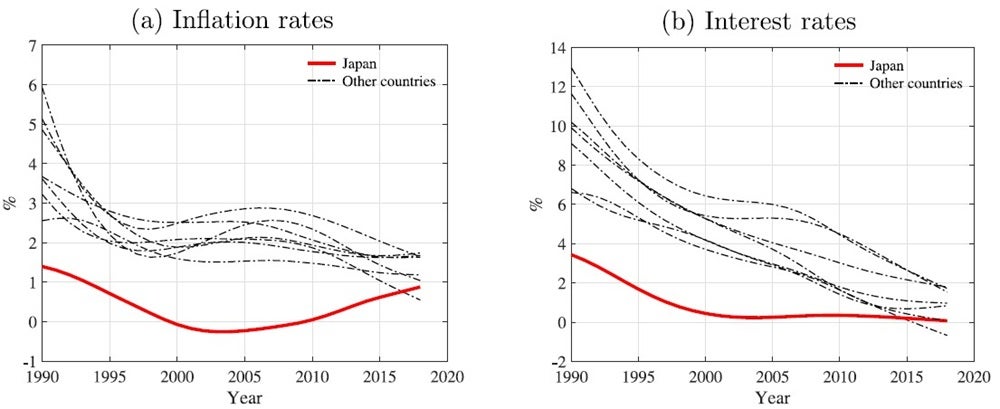

Japan told the same story from the opposite direction. The Bank of Japan held rates at or near zero for three decades, and inflation stayed low the entire time – exactly as the theory predicted. The paper identified Japan as a clear outlier among OECD nations, with interest rates and inflation both persistently below those of its peers. It warned that if low nominal interest rates were maintained, deflation was likely to return.

Interest rate lessons for business and Australia

For business leaders, the takeaway of the research is that quarterly CPI surprises, hawkish press conferences and shipping disruptions mattered far less over the medium term than the direction of central bank policy.

The research also offered a lesson for the current debate: when fighting inflation, it was “better to go for higher rates rather than to keep them high for longer.” The latter approach risked transforming a temporary tightening into something markets interpreted as a shift in the inflation target – with consequences that extended well beyond the next quarter.

Learn more: How inflation is measured (and why it hits harder at Christmas)

Dr Gao concluded by pointing to the RBA’s recent decisions to increase cash rates. “If this rebound continues, further tightening may be hard to avoid. The critical distinction now is not simply whether rates rise, but how the move is framed: a short, targeted increase to stabilise prices carries very different implications from a clear signal that borrowing costs will remain elevated for an extended period,” said Dr Gao.

“A ‘higher for longer’ stance can look like a more permanent shift in the policy regime – and that, in turn, can influence medium-term inflation expectations. So, the real question for markets and businesses alike is this: will the RBA opt for a brief squeeze, or are we witnessing a longer reset in Australia’s rate environment?”