What really drives foreign exchange rates?

Research shows forex markets follow daily patterns around fixing times, with implications for currency risk, trading strategies and US dollar demand

This article is republished with permission from China Business Knowledge, the knowledge platform of Chinese University of Hong Kong (CUHK) Business School. You may access the original article here.

Foreign exchange or forex is the largest and most liquid financial market in the world, with a daily trading volume of US$9.6 trillion, according to a 2025 survey by the Bank for International Settlements. This number is significantly higher than the stock markets, which are estimated to be around US$700 billion per day.

Forex traders buy and sell currencies to profit from differences in exchange rates across a global, decentralised market. With low capital requirements and the flexibility to trade anywhere, forex trading may appear easy, but practice suggests otherwise. The forex market is highly volatile and influenced by global politics and economics.

Although various methods have been designed to anticipate price movements and manage risk, forex traders suffering huge losses are not uncommon sights. A notable example is the US$900 million loss suffered by world-renowned investor Warren Buffett in 2005, which signals the unpredictable nature of foreign currency investment.

As the most widely traded currency, the US dollar is involved in more than 80 per cent of all forex transactions. Some argue that this domination may change amid intensifying trade and geopolitical tensions, along with US tariffs and protectionist policies that could potentially weaken the greenback’s hegemonic position.

However, Paul Whelan, Associate Professor in the Department of Finance at the Chinese University of Hong Kong (CUHK) Business School, remains cautious about anticipating dramatic changes to established patterns. “It’s too early to know if US tariffs will change the norm. The fundamental driver, consistent global demand for US dollar-denominated assets, remains robust despite shifting geopolitical dynamics.”

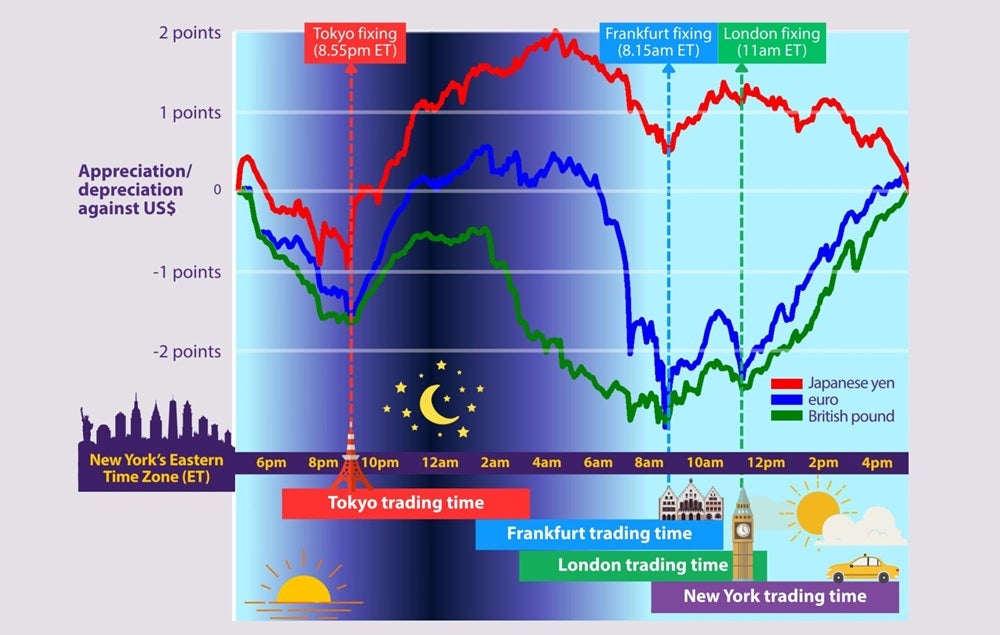

Although predicting currency market movements accurately is impossible, Professor Whelan’s recent study reveals a fascinating cycle that also demonstrates the persistent appeal of the US dollar. Every day at precisely 9.55am in Tokyo, 2.15pm in Frankfurt, and 4pm in London, the US dollar strengthens dramatically, only to weaken just afterwards. It’s a systematic pattern researchers have now quantified, revealing daily swings exceeding US$1 billion across global currency markets.

“Rather than market inefficiency, we find the daily swing pattern as a structural feature of the currency market driven by the prevalent demand for US dollars,” Professor Whelan says.

What causes the billion-dollar daily swing pattern?

In a paper titled Foreign exchange fixings and returns around the clock, Professor Whelan, along with Ingomar Krohn at the Bank of Canada and Philippe Mueller at Warwick Business School, examined 21 years of high-frequency trading data and discovered a daily swing pattern around specific moments known as fixings. Fixings refer to the times when currency exchange rates are officially published, calculated by aggregating bids and offers to establish a reference price for valuing and executing international transactions.

Several key fixings are used worldwide, but the most prominent ones are the Tokyo, Frankfurt and London fixings, which have provided benchmarks for major currencies such as the yen, euro and pound, the top three currencies traded against the US dollar. Banks in Tokyo simultaneously publish their fixing at 9.55am, Frankfurt-headquartered European Central Bank announces its fixing at 2.15pm, and London-based Thomson Reuters updates its WM/Reuters fixing at 4pm, all in local time.

If converted to New York’s Eastern Time Zone (ET), Tokyo fixing happens at 8.55pm, Frankfurt at 8.15am, and London at 11am ET. As shown below, these fixing times are not exactly aligned, creating W-shaped patterns where the US dollar appreciates before the fixings and depreciates immediately afterwards.

Foreign currencies vs US dollar patterns across different fixings in 24 hours

Tokyo fixing is especially important as Japan doesn’t apply daylight saving time, a common practice among Northern Hemisphere countries where the clocks are set forward by one hour in spring and back by one hour in autumn, resulting in a change in time difference between Tokyo and other cities in the study throughout the year. From spring through autumn, the W-shaped pattern near the Tokyo fixing shifts by about one hour.

“Japan’s non-observance of daylight savings time serves as a quasi-natural experiment to prove the reversal is really tied to the fixing time,” says Professor Whelan.

What makes the finding striking is its consistency. The analysis of the nine most frequently traded currencies against the US dollar reveals a pervasive, highly statistically significant daily pattern across different time periods, suggesting that this isn’t a temporary market quirk but a fundamental feature of how global currency markets operate.

The researchers believe that the pattern is driven by demand for US dollars at around major currency fixing times. Traders and financial institutions that facilitate foreign exchange transactions accumulate US dollars to meet this demand, thereby driving the greenback higher against other currencies. Right after the fixings, the dollars are sold back, leading to a price drop.

Learn more: Foreign banks and credit booms: Hidden harbingers of financial crises?

These findings highlight important considerations for managing currency risk. For corporations holding international operations, the real-world implications are significant. “Cross-border businesses might take into account timing around fixings to address pricing uncertainty,” says Professor Whelan.

Currency markets don’t always follow the logic

While identifying the daily swing pattern may help mitigate investment risk, it is worth noting that foreign exchange remains volatile due to the significant influence of external factors and trading behaviours. Another study by the researchers, Uncovered interest parity in high frequency, highlights that currency markets are not perfectly rational or predictable.

The researchers explore an investment strategy called a carry trade, which involves borrowing in low-interest-rate currencies, such as the Japanese yen, to invest in assets denominated in higher-interest-rate currencies, like the US dollar. According to the uncovered interest rate parity (UIP) theory, exploiting the interest rate differential shouldn’t yield consistent profits, as currencies with higher interest rates should gradually depreciate to offset the interest gains and maintain market balance.

However, the fact that some traders can still make profits from a carry trade has been perplexing. The researchers sought to determine how and when such an anomaly occurs by analysing foreign exchange market data spanning more than 25 years, focusing on nine of the most heavily traded currencies that account for 75 per cent of global daily average trading volume.

Subscribe to BusinessThink for the latest research, analysis and insights from UNSW Business School

The results show that when major currency markets are closed or less active, mostly at night, the UIP theory tends to hold in diminishing carry trades. However, during the day at US trading hours, currencies with higher interest rates tend to appreciate rather than depreciate, which contradicts the UIP theory. Most of the profits from carry trades are actually made in short bursts when major economic news comes out, such as the Federal Reserve’s announcements or major economic reports, during trading hours.

“Important economic news, like major reports or announcements, can cause sudden and big changes in currency prices as they show whether the economy is doing well or poorly,” says Professor Whelan. “Holding onto currency investments during these times is risky because prices can jump unexpectedly. To be willing to take this risk, investors need to expect higher returns as compensation for facing these shocks.”

On average, big news days account for only 17 per cent of all trading days in the sample, but contribute to two-thirds of the extra profit beyond normal market fluctuations. However, the probability of losses remains non-negligible, particularly during periods of market turbulence or when currencies behave abnormally.

Currency markets are more nuanced and less predictable compared to other financial markets. While classical theories provide a helpful framework, real-world data reveal consistent patterns of deviations. Market expectations and reactions are vital in understanding currency movements, more crucial than relying on interest rate differentials.